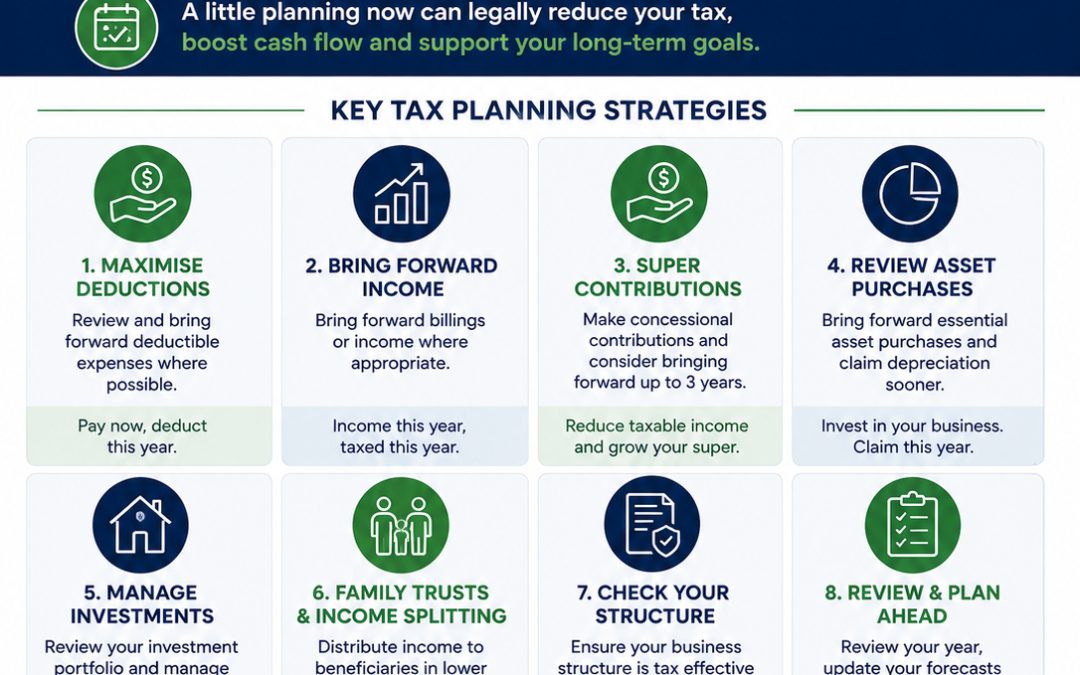

As the end of the financial year approaches, Australians have a valuable opportunity to review their tax position and implement strategies that could legally reduce tax and strengthen long-term wealth.

Two of the most effective year-end tax planning areas in 2026 are maximising superannuation contributions and reviewing family trust distributions before 30 June. Both strategies can provide substantial tax benefits when handled correctly, but strict contribution caps and timing rules apply. Planning before year end allows individuals, business owners and families to take advantage of government incentives, reduce taxable income, and position themselves more effectively for the future.

Why Superannuation Remains One of Australia’s Best Tax Strategies

Superannuation continues to be one of the most tax-effective wealth creation tools available to Australians.

The government actively encourages retirement savings by offering concessional tax treatment on contributions and investment earnings inside super. However, many Australians still fail to fully utilise the available contribution limits and government incentives before 30 June. For many taxpayers, EOFY is the ideal time to review whether additional super contributions could reduce tax while boosting long-term retirement savings.

Super Contribution Caps for 2025–26

There are two main categories of super contributions:

Tax-Deductible Super Contributions

These include:

- Employer super guarantee contributions

- Salary sacrifice contributions

- Personal deductible contributions claimed at tax time

The concessional contribution cap for the 2025–26 financial year is:

- $30,000 per person

From 1 July 2026, this cap will increase to:

- $32,500 per person

Exceeding the cap may trigger additional tax, making careful planning essential before making extra contributions.

Non-Concessional Super Contributions

These are personal contributions made from after-tax savings where no tax deduction is claimed.

The current annual non-concessional contribution cap is:

- $120,000 per person

From 1 July 2026, the cap increases to:

- $130,000 per person

These contributions can be particularly useful for individuals looking to build retirement savings or contribute proceeds from investments or asset sales into the superannuation environment.

The Power of Starting Super Contributions Early

One of the greatest advantages of superannuation is the power of long-term compound growth. Money invested inside super benefits from a concessional tax environment, allowing earnings to compound more effectively over time.

Example: The Impact of Time on Super Growth

If $100,000 is contributed into super at age 25 and earns an average annual return of 7%, it could grow to approximately:

- $1.5 million by age 65

However, if the same $100,000 is contributed at age 40, it may only grow to:

- Around $542,000 by retirement

The difference of almost $1 million highlights how valuable early contributions can be for long-term retirement outcomes.

Super Contribution Splitting with Your Spouse

Many Australians are unaware they can split certain super contributions with their spouse.Under contribution splitting rules, a super fund may transfer up to 85% of eligible concessional contributions made in the previous financial year into a spouse’s super account.

This strategy can help:

- Balance super balances between spouses

- Improve future retirement planning flexibility

- Assist with transfer balance cap management later in life

Importantly, spouses can hold different super funds and still utilise this strategy. Applications generally need to be completed before 30 June each year.

The Government Super Co-Contribution: Free Money for Eligible Australians

The government continues to offer one of Australia’s most underutilised super incentives — the super co-contribution. If your income is below $62,488 in 2025–26, you may qualify for a government contribution by making a personal after-tax contribution into super.

How the Super Co-Contribution Works

- Contribute $1,000 into super from your own savings

- Do not claim a tax deduction

- The government may contribute up to $500 directly into your super account

The full $500 co-contribution applies for individuals earning under $37,000 and phases out gradually above this level. For younger Australians, even small contributions can produce significant long-term results through compound growth.

Spouse Super Contributions and Tax Offsets

If your spouse earns less than $40,000 annually, contributing to their super may also provide a personal tax offset.

How the Spouse Contribution Offset Works

You can contribute up to:

- $3,000 into your spouse’s super account

In return, you may receive:

- An 18% tax offset

- Worth up to $540

This strategy helps increase household retirement savings while also delivering an immediate tax benefit.

Why EOFY Super Planning Matters

Superannuation rules become increasingly complex when factors such as:

- Taxable income

- Existing super balances

- Age

- Contribution history

- Total super balance thresholds

are taken into account. Reviewing contribution opportunities before 30 June allows time to structure contributions correctly and avoid missing valuable tax-saving opportunities.

Family Trust Distributions 2026: What You Need to Know Before 30 June

For families operating discretionary or family trusts, April, May and June are critical planning months. Trust distribution decisions must generally be made before 30 June each year, and failing to do so correctly can result in significant tax consequences.

How Family Trusts Are Taxed in Australia

Under Australian tax law, trust income is generally taxed once only.

Either:

- The beneficiaries pay tax on distributed income, or

- The trust itself pays tax

However, if the trust is taxed directly, the tax rate can reach:

- 47% including Medicare levy

This is why distributing income to beneficiaries on lower marginal tax rates is often far more tax effective.

Choosing the Right Beneficiaries for Trust Distributions

Effective family trust tax planning often involves distributing income to family members with lower taxable incomes.

Potential beneficiaries may include:

- Adult children studying at university

- A lower-income spouse

- Retired parents

- Adult family members with lower taxable income

By distributing income strategically, families may significantly reduce their overall tax burden.

Trust Distribution Rules Are Strict

The ATO closely monitors trust distributions and anti-avoidance rules apply.Distributions must be genuine, and beneficiaries must actually receive or benefit from the income allocated to them. Simply allocating income on paper without genuine entitlement can trigger ATO scrutiny and potential penalties.

When Paying Higher Tax Through the Trust May Still Make Sense

Although distributing trust income is usually preferable, there are situations where retaining some income inside the trust and paying tax at the top marginal rate may be appropriate.

For example:

- Additional income may push a beneficiary into a higher tax bracket

- It could impact HELP debt repayments

- Family assistance payments or Medicare surcharges may be affected

- Division 293 tax thresholds may apply

Effective tax planning considers the broader financial picture rather than simply chasing the lowest immediate tax rate.

The 30 June Deadline for Family Trust Distributions

One of the most important rules for discretionary trusts is that distribution decisions must generally be documented before 30 June. There is no flexibility once the financial year ends. Waiting until after year end to decide who should receive trust income is often too late.

Proper planning requires:

- Reviewing estimated trust income before year end

- Determining the most tax-effective distribution strategy

- Preparing trustee resolutions before 30 June

Failing to act in time can expose trust income to the top marginal tax rate.

Conclusion: EOFY Tax Planning Can Deliver Significant Savings

EOFY tax planning is about far more than simply lodging a tax return. Proactive planning before 30 June can create substantial opportunities to legally minimise tax, increase retirement savings and improve long-term wealth outcomes.

Maximising superannuation contributions, utilising government incentives, reviewing spouse contribution strategies, and carefully planning family trust distributions are some of the most effective strategies available to Australian taxpayers in 2026.

Because contribution caps, trust rules and tax thresholds can become highly complex, seeking professional advice before year end can help ensure strategies are implemented correctly and deadlines are not missed.

How can we help?

If you have any questions or would like further information, please feel free to give our office on 08 9221 5522 or via email – info@camdenprofessionals.com.au or arrange a time for a meeting so we can discuss your requirements in more detail.

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on this website, Camden Professionals, its officers, representatives, employees, and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.

Recent Comments