by Camden Professionals | Jun 23, 2026 | Division 7A Rules, Trusts

Landmark High Court Victory for Trusts and Private Groups The High Court’s decision in Commissioner of Taxation v Bendel [2026] HCA 18 is one of the most significant tax cases affecting trusts and private groups in recent decades. In a decisive 5-2 majority...

by Camden Professionals | May 27, 2026 | Capital Gains Tax (CGT), Federal Budget 2026 -2027, Property Investment, Property Investment Tips, Trusts

For decades, Australian property investors have relied on discretionary trusts and companies to build wealth, protect assets, and improve tax outcomes. These structures were often promoted as powerful tools for income streaming, estate planning, asset protection and...

by Camden Professionals | May 21, 2026 | Family Trusts, Trust Distribution Resolutions 2026, Trusts

For many Australian business owners and investors, discretionary trusts remain one of the most effective structures for managing wealth, protecting assets and creating tax flexibility. However, that flexibility comes with strict timing requirements — particularly when...

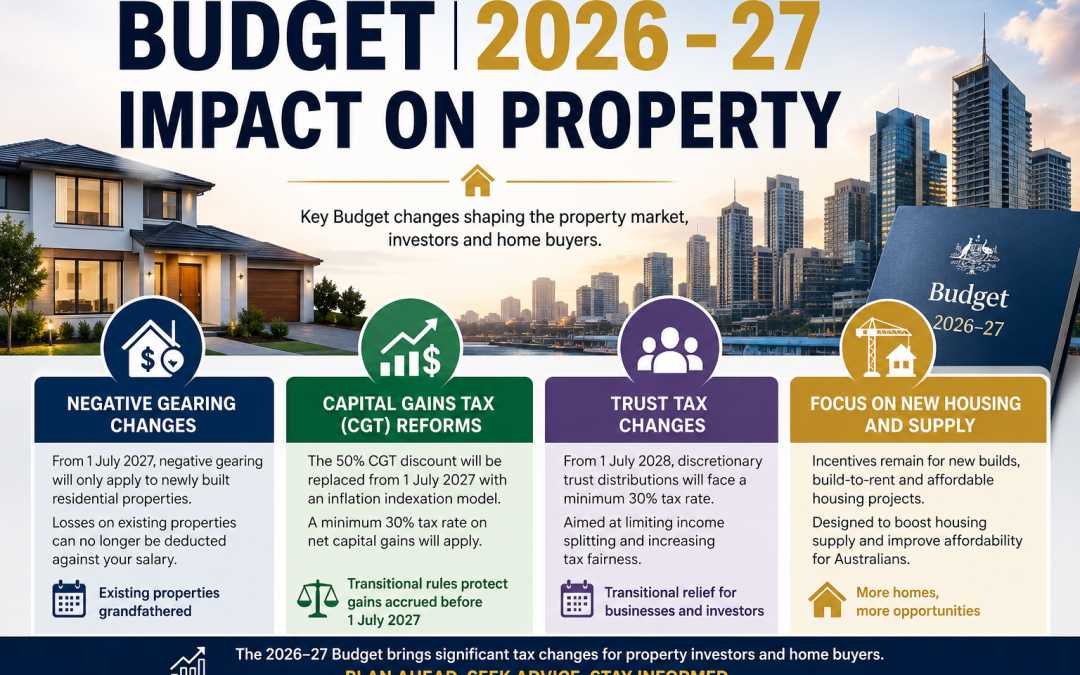

by Camden Professionals | May 13, 2026 | Capital Gains Tax (CGT), Federal Budget 2026 -2027, Negative Gearing, Trusts

The 2026 Australian Federal Budget handed down on 12 May 2026 introduced some of the most significant investment tax reforms in decades. The Albanese Government announced sweeping changes to negative gearing, capital gains tax (CGT), and discretionary trusts as part...

by Camden Professionals | Apr 29, 2025 | Foreign Investors, Property Investment, Trusts

Trusts are a common investment vehicle in Australia, particularly for groups of investors seeking to pool funds into passive income-generating assets such as property or infrastructure. For tax purposes, trusts are typically treated as flow-through entities, meaning...

by Lilian Fisher | Mar 24, 2025 | ATO, Division 7A Rules, Trusts

Since 16 December 2009, the Australian Taxation Office (ATO) has maintained the view that when a family trust appoints income to a corporate beneficiary (referred to as the beneficiary company) without making a payment, the unpaid present entitlement (UPE) constitutes...

Recent Comments