Australia’s property investment landscape has shifted dramatically following the 2026–27 Federal Budget delivered on 12 May 2026. The Federal Government announced sweeping reforms targeting negative gearing, capital gains tax (CGT), discretionary trusts and investment property concessions changes that are expected to significantly affect property renovators, flippers and developers.

At the same time, the ATO has intensified compliance activity around property transactions, GST obligations and profit-making property ventures.

For investors undertaking renovations, subdivision projects, duplex builds or short-term property flips, understanding how these new rules interact with existing ATO guidelines has become critical.

The difference between capital account treatment, ordinary income treatment and carrying on a property development business can now have a major impact on tax payable, access to deductions, GST obligations and overall profitability.

The 2026 Federal Budget: Major Tax Changes for Property Investors

The 2026–27 Federal Budget introduced some of the most significant property tax reforms in decades.

According to the official Federal Budget papers, the Government announced that negative gearing concessions for residential property will largely be limited to newly constructed properties from 1 July 2027. Existing investment properties held before Budget night are expected to be grandfathered under the current rules.

The Budget also confirmed major changes to capital gains tax treatment, replacing the long-standing 50% CGT discount model with an inflation-indexation approach for future investments.

In addition, discretionary trusts are expected to face new minimum tax rules and greater scrutiny around income distributions.

These reforms are aimed at:

- Redirecting investor demand toward new housing supply

- Improving housing affordability

- Reducing speculative investment activity

- Increasing tax integrity and compliance

- Raising additional government revenue

For property investors, the changes substantially alter the tax outcomes of renovation and development strategies.

Negative Gearing Changes and Property Investment

One of the biggest changes announced in the Budget relates to negative gearing.

Under the proposed reforms:

- Existing property investors who owned investment properties before Budget night are expected to retain current concessions

- New negative gearing benefits after 1 July 2027 will generally apply only to newly built residential properties

- Existing established properties purchased after the commencement date may no longer allow investors to offset rental losses against salary and wage income

The Government argues these changes are designed to encourage investment into new housing stock rather than established dwellings.

What This Means for Renovators and Flippers

The distinction between renovating an existing property and constructing new dwellings has become increasingly important.

For example:

- Cosmetic renovations to an existing dwelling may not qualify for the new-build concessions

- Substantial redevelopment projects involving new construction may still access favourable treatment

- Knockdown-rebuild projects may face complex eligibility rules

As a result, investors engaging in renovation and resale activities must carefully assess whether their projects qualify as “new residential premises” for tax purposes.

Capital Gains Tax (CGT) Changes After the Budget

Historically, Australian investors who held property for more than 12 months could access the 50% CGT discount.

The 2026 Federal Budget significantly reshapes this framework.

Under the proposed reforms:

- The 50% CGT discount will be replaced for future investments

- A new inflation-indexation model will apply to capital gains

- Transitional rules are expected to apply for existing holdings

- A minimum effective tax rate on certain gains may apply

These changes are intended to reduce speculative investment and reduce reliance on capital growth strategies.

Property Flipping: Why Many Investors Lose CGT Concessions

Many investors mistakenly assume that all property profits qualify for capital gains treatment.

However, the ATO has consistently maintained that where a property is acquired with a profit-making intention, the profits may instead be treated as ordinary income.

The ATO’s property renovation guidance states that tax outcomes depend on whether the taxpayer is:

- A passive investor

- Engaged in a profit-making undertaking

- Carrying on a business of property development or renovation

- If a project is classified as a profit-making venture:

- The 50% CGT discount may not apply

- Profits are taxed at marginal tax rates

- GST obligations may arise

- The activity may be treated as a business

Example: The Property Flipper

An investor purchases a distressed property, renovates it over six months and sells it for a substantial profit.Even if this is a one-off transaction, the ATO may determine the property was acquired primarily for resale profit.

In that situation:

- The gain may be taxed as ordinary income

- CGT concessions may be denied

- The main residence exemption may not apply

- GST may become relevant if substantial renovations occurred

The ATO has indicated that repeated flipping activity is now an increased compliance focus.

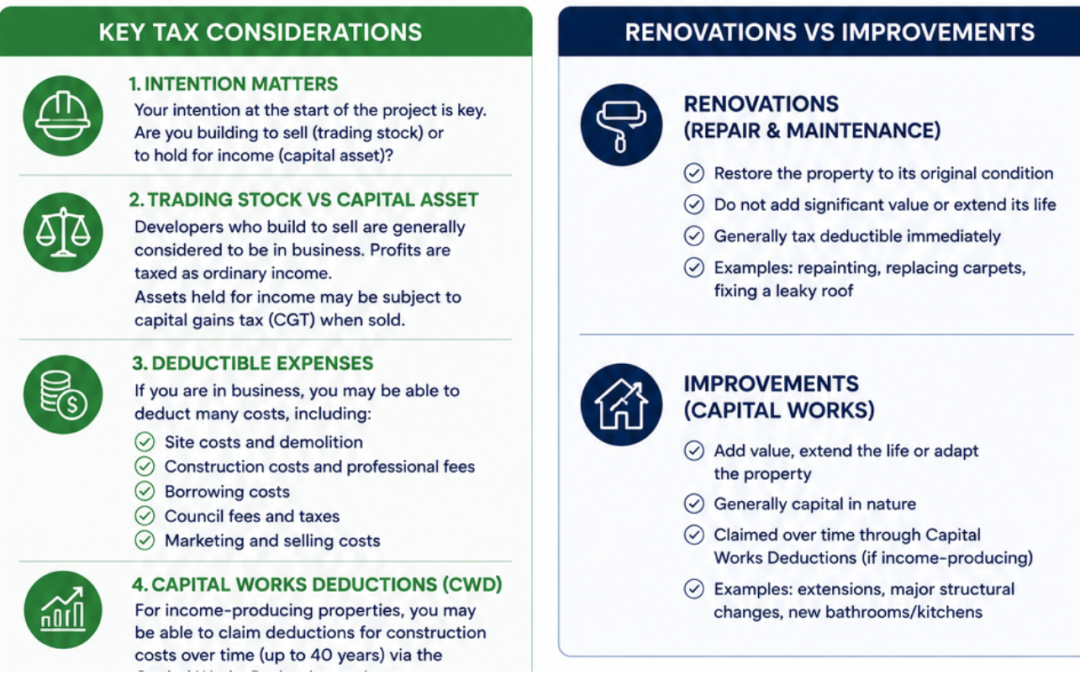

Renovation Tax Rules: Repairs vs Capital Improvements

For long-term investors holding rental properties, renovation expenses are not automatically deductible.

The tax treatment depends on whether the expenditure is:

- Repairs and maintenance

- Initial repairs

- Capital improvements

According to ATO guidance:

- Repairs restoring an existing item may be immediately deductible

- Structural upgrades or improvements are generally capital in nature

- Capital works deductions may apply over time

- Remaining costs form part of the CGT cost base (Australian Taxation Office)

Common ATO Audit Area

The ATO closely reviews investors who incorrectly classify capital improvements as immediate repairs.

Examples of capital improvements include:

- Kitchen replacements

- Bathroom upgrades

- Structural extensions

- New roofing

- Major landscaping projects

These costs generally cannot be fully deducted upfront.

Property Development and GST Obligations

Once projects become larger or more commercial, the tax treatment becomes significantly more complex.

Activities commonly treated as property development enterprises include:

- Duplex construction

- Townhouse developments

- Subdivisions

- Multi-dwelling projects

- Land development for resale

Under ATO rules, the sale of new residential premises is generally subject to GST.

This means developers may need to:

- Register for GST

- Lodge Business Activity Statements (BAS)

- Account for GST on sales

- Apply the margin scheme correctly

- Maintain extensive project records

The Margin Scheme

The margin scheme allows GST to be calculated on the “margin” rather than the full sale price of eligible developments.This can substantially reduce GST payable.

However:

- Eligibility depends on acquisition history

- Contracts must specifically allow the margin scheme

- It cannot normally be applied retrospectively

- Incorrect documentation can invalidate eligibility.GST mistakes remain one of the biggest financial risks for inexperienced property developers.

Trusts and Property Development After the 2026 Budget

Discretionary trusts have long been popular for property development and asset protection strategies.However, the 2026 Federal Budget proposes increased taxation and scrutiny of trust distributions.

According to budget commentary and Treasury announcements:

- New minimum tax rules may apply to discretionary trust income

- Distribution splitting strategies may face tighter limits

- Property development profits distributed through trusts may attract increased review

- ATO compliance activity involving trusts is expected to increase substantially

Why Trusts Still Matter

Despite increased scrutiny, trusts may still offer advantages including:

- Asset protection

- Estate planning flexibility

- Income distribution flexibility

- Joint venture structuring

- Separation of development risk

However, investors now need to carefully assess whether companies, trusts or hybrid structures are more appropriate under the new rules.

Interest Deductibility and Changing Intentions

A major risk area for property investors is where the intention of a project changes over time.

For example:

- A property initially acquired as a long-term rental may later become a development project

- An investor may decide to subdivide land or construct townhouses

- A “buy-and-hold” strategy may evolve into a resale strategy

When intention changes:

- Interest deductibility may change

- Trading stock rules may apply

- GST obligations may arise

- Tax treatment can shift from capital account to revenue account

This area has become a major focus for the ATO following increased compliance funding announced in the Budget.

Increased ATO Compliance and Data Matching

The ATO now uses extensive data matching across:

- State land titles offices

- Banks and lenders

- Airbnb-style platforms

- Building approvals

- AUSTRAC reporting

- Rental bond authorities

- Solicitor settlement data

Property investors undertaking undeclared flipping or development activities face increasing audit exposure.

The ATO is particularly focused on:

- Undeclared property profits

- Incorrect CGT claims

- Main residence exemption abuse

- GST avoidance

- Trust distribution arrangements

- Cash payments to contractors

- Incorrect repair deductions

Final Thoughts

The 2026 Federal Budget has fundamentally reshaped the tax environment for Australian property investors.Negative gearing reforms, CGT changes and new trust taxation measures mean renovation, flipping and development projects now require far more careful planning than in previous years.

At the same time, the ATO has significantly expanded its compliance focus around property-related activities.

Investors undertaking renovations, subdivisions or development projects should obtain professional advice before commencing projects to ensure they:

- Structure projects correctly

- Understand GST obligations

- Maximise legitimate deductions

- Manage trust distribution risks

- Avoid losing CGT concessions

- Remain compliant with evolving tax laws

With billions of dollars in additional compliance funding now directed toward property tax enforcement, proactive planning is becoming essential rather than optional.

Frequently Asked Questions (FAQs)

Will negative gearing be abolished in Australia?

No. Under the 2026 Federal Budget proposals, negative gearing is expected to remain available for newly constructed residential properties, while existing investment properties held before Budget night are expected to be grandfathered.

Are property flipping profits subject to CGT?

Not always. If the ATO determines the property was acquired with the intention of resale for profit, the profits may be taxed as ordinary income instead of capital gains.

Can I still use a trust for property development?

Yes, but trusts are expected to face greater scrutiny and potentially new minimum tax rules following the 2026 Budget reforms.

Does GST apply to property developments?

Generally yes, where new residential premises are sold or substantial renovations occur.

What is the margin scheme?

The margin scheme allows GST to be calculated on the profit margin rather than the full sale price, potentially reducing GST payable.

Will the 50% CGT discount still exist?

The 2026 Budget proposes replacing the existing 50% CGT discount with an inflation-indexation model for future investments. Transitional rules are expected for existing assets.

Can renovation expenses be immediately deducted?

Only genuine repairs and maintenance are generally immediately deductible. Capital improvements are usually depreciated or added to the CGT cost base.

Why is the ATO targeting property investors?

The Government has expanded ATO compliance funding to improve tax integrity, increase revenue collection and address perceived misuse of property-related tax concessions.

Sources:

- ATO

- Budget Papers 2026-7

- The Guardian

How can we help?

If you have any questions or would like further information, please feel free to give our office on 08 9221 5522 or via email – info@camdenprofessionals.com.au or arrange a time for a meeting so we can discuss your requirements in more detail.

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on this website, Camden Professionals, its officers, representatives, employees, and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.

Recent Comments