The 2026 Australian Federal Budget handed down on 12 May 2026 introduced some of the most significant investment tax reforms in decades. The Albanese Government announced sweeping changes to negative gearing, capital gains tax (CGT), and discretionary trusts as part of a broader strategy to improve housing affordability and rebalance the tax system.

The reforms are expected to raise billions in additional revenue over the next decade while reshaping how Australians invest in property and structure wealth.

For investors, business owners and high-income earners, understanding the proposed changes is critical.

Negative Gearing Changes in the 2026 Federal Budget

What Is Negative Gearing?

Negative gearing occurs when the costs of holding an investment asset exceed the income it generates. Traditionally, Australians have been able to offset those losses against salary and wage income, reducing their overall tax bill.

For decades, this has been one of the most powerful tax strategies available to property investors.

What Has Changed?

Under the 2026 Federal Budget reforms:

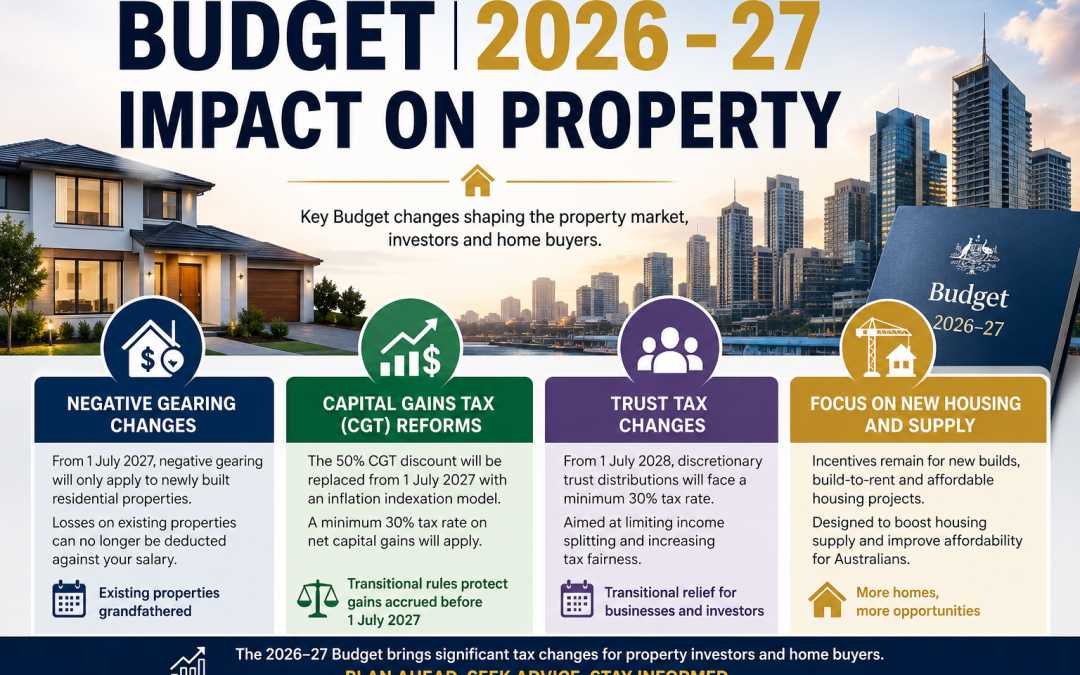

- From 1 July 2027, negative gearing will generally only apply to newly built residential properties

- Existing investment properties owned before Budget night on 12 May 2026 will be grandfathered

- Investors purchasing established homes after Budget night will no longer be able to offset rental losses against wage income

- Losses on established properties can only be offset against future residential investment income or carried forward

- Build-to-rent projects, affordable housing projects and some institutional investors remain exempt

The Government says the reforms are designed to redirect investor demand toward increasing housing supply rather than competing with owner-occupiers for existing homes.

Example: Impact of the New Negative Gearing Rules

Current Rules

Susan earns a salary of $190,000 per year and owns an investment property.

- Rental income: $800 per week

- Property expenses: $1,000 per week

- Annual loss: $10,400

Under the current rules, Susan deducts the $10,400 loss against her salary income.

This reduces her taxable income and saves approximately $4,856 in tax annually.

Under the New Rules

If Susan buys an established property after 12 May 2026 and the rules commence from 1 July 2027:

- She can no longer offset the $10,400 loss against her salary

- The loss can only offset future rental profits or future capital gains from property investments

- Her immediate annual tax saving disappears

For many investors, this significantly reduces the cash flow attractiveness of purchasing older investment properties.

Who Benefits and Who Loses?

Likely Winners

- First-home buyers

- Developers of new housing

- Investors purchasing new builds

Likely Losers

- Investors targeting established properties

- High-income earners using tax deductions to reduce PAYG tax

- Property markets heavily reliant on investor activity

Treasury estimates the changes could improve housing accessibility for younger Australians while increasing federal revenue over time.

Capital Gains Tax Changes Explained

How the Current CGT Discount Works

Since 1999, Australians who hold an asset for more than 12 months only pay tax on 50% of the capital gain.

This discount applies to:

- Investment properties

- Shares

- Managed funds

- Other CGT assets

Critics argue the 50% discount has fuelled property speculation and disproportionately benefited wealthier Australians. Treasury estimates the CGT discount costs approximately $21.8 billion annually in forgone revenue.

What Is Changing in 2026?

The Federal Budget announced that from 1 July 2027:

- The 50% CGT discount will be replaced with an inflation indexation model

- Investors will only be taxed on “real” gains after inflation

- A minimum 30% tax rate on net capital gains will apply

- Existing gains accrued before 1 July 2027 will remain protected under transitional arrangements

- Investors in new residential builds may choose between the old 50% discount or the new indexation method

Example: Current CGT Rules vs New Rules

Current Rules

Wayne buys an investment property for $500,000 and sells it for $700,000.

Capital gain = $200,000

Under the current 50% discount:

- Taxable gain = $100,000

- If Wayne earns $190,000 annually, the gain is taxed at 45%

- Approximate CGT payable = $45,000 plus Medicare levy

Under the New Budget Rules

Assume inflation averages 5% annually over three years.

Indexed cost base becomes approximately $579,000.

Real capital gain becomes approximately $121,000.

At the proposed minimum 30% CGT rate:

- Tax payable = approximately $36,300 minimum

- If Wayne’s marginal rate exceeds 30%, tax may be higher depending on final legislation

The new system favours lower-growth, inflation-driven assets while reducing tax advantages from rapid speculative price increases.

Key Investor Implications

Higher Complexity

Investors will now need to:

- Track inflation-adjusted cost bases

- Calculate gains before and after July 2027

- Potentially maintain dual CGT calculations

Reduced Incentive for Speculative Property Investment

The combination of:

- restricted negative gearing

- reduced CGT concessions

- minimum tax rates

may reduce the attractiveness of leveraged property investing strategies.

Increased Focus on New Housing Supply

The Government is clearly attempting to redirect investor capital into:

- new residential developments

- build-to-rent projects

- affordable housing initiatives

Trust Tax Changes in the 2026 Federal Budget

Why Trusts Are Under Scrutiny

Discretionary family trusts have long been used by higher-income families to distribute income to beneficiaries on lower tax rates.

The Government argues that trusts have increasingly been used to minimise tax rather than simply manage family assets.

The Budget papers noted that more than 90% of private trust wealth is held by the top 10% of households.

What Is Changing?

From 1 July 2028, the Government plans to introduce:

- A minimum 30% tax rate on discretionary trust distributions

- Restrictions on income splitting to low-income adult beneficiaries

- Transitional restructuring periods for some small businesses and investors

Example: How the Trust Changes Could Work

Gerard operates his plumbing business through a discretionary family trust.

Current income:

- Gerard: $230,000 business income

- Wife: not working

- Adult son: earns $10,000 annually

Current Rules

The trust distributes income among family members:

- Gerard receives $120,000

- Wife receives $60,000

- Son receives $50,000

This reduces the family’s total tax bill from approximately $69,600 to around $44,400.

Under the Proposed Rules

If trust distributions become subject to a minimum 30% tax:

- Much of the tax advantage from splitting income disappears

- The family may pay significantly higher overall tax

- Some business owners may consider restructuring into companies or fixed trusts

What Business Owners Should Consider

Business owners and investors using trusts should review:

- Existing trust structures

- Succession planning arrangements

- Asset protection strategies

- Company vs trust tax structures

- Future distribution flexibility

The reforms could have major implications for SMEs, professional service firms, property investors and high-net-worth families.

What the 2026 Budget Means for Investors

The 2026 Federal Budget represents a major philosophical shift in Australian tax policy.

The Government is effectively reducing tax concessions tied to passive asset growth while redirecting incentives toward:

- new housing supply

- wage earners

- productive investment

The reforms remain subject to legislation and political negotiation, but they signal a significant change in how wealth creation through property and investment assets will be taxed in Australia.

For investors, business owners and trustees, early tax planning will become increasingly important over the next 12 to 24 months.

Key Dates to Watch

| Measure | Commencement Date |

| Negative gearing restrictions | 1 July 2027 |

| CGT discount replacement | 1 July 2027 |

| Minimum CGT tax rules | 1 July 2027 |

| Trust minimum tax rules | 1 July 2028 |

Sources:

- Budget Papers 2026 – 27

- Treasury- Budget Tax Reforms

- Reuters

How can we help?

If you have any questions or would like further information, please feel free to give our office on 08 9221 5522 or via email – info@camdenprofessionals.com.au or arrange a time for a meeting so we can discuss your requirements in more detail.

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on this website, Camden Professionals, its officers, representatives, employees, and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.

Recent Comments