One of the most common questions Australians ask at tax time is, “What’s the difference between a tax deduction and a tax offset?”

While both can reduce the amount of tax you pay, they work in very different ways. Understanding the distinction is important because many taxpayers mistakenly believe they provide the same benefit or that every expense automatically results in a dollar-for-dollar reduction in tax.

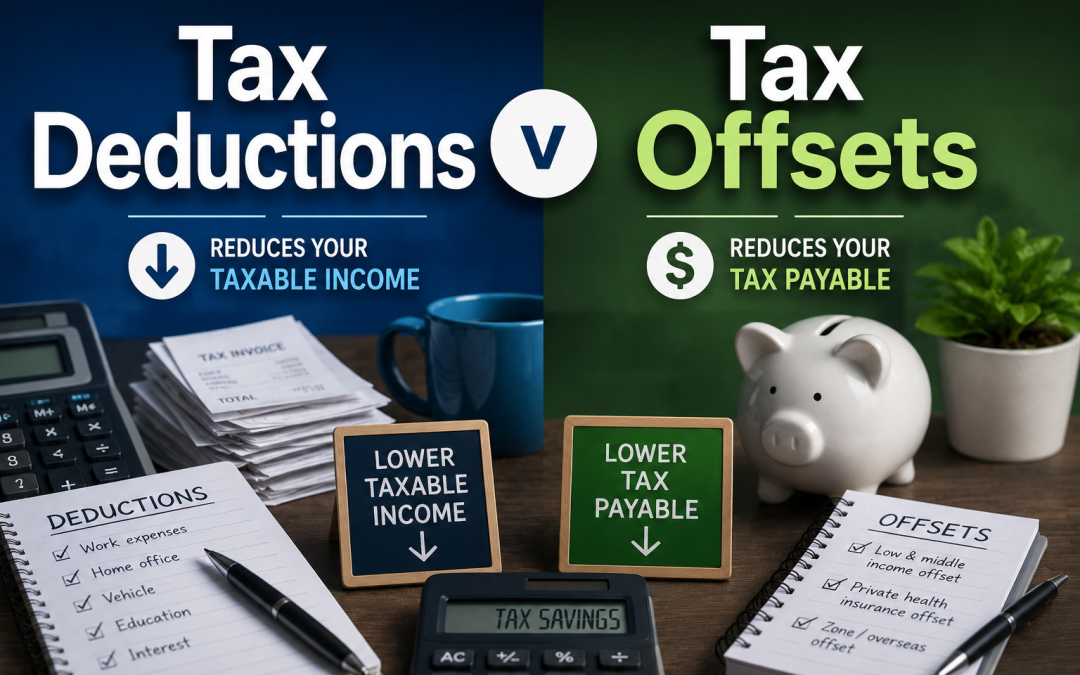

The Australian Taxation Office (ATO) regularly reminds taxpayers that deductions reduce your taxable income, while tax offsets reduce the tax payable after your tax has been calculated. Knowing how each works can help you better understand your tax return, avoid common misconceptions and ensure you’re claiming all the benefits you’re entitled to. In this guide, we’ll explain how tax deductions and tax offsets work, provide practical examples, outline common tax offsets available to Australians and discuss why understanding the difference can make tax time less confusing.

What Is a Tax Deduction?

A tax deduction is an expense that reduces your taxable income.

Rather than reducing your tax bill directly, a deduction lowers the amount of income the ATO uses to calculate how much tax you owe.

For example:

- Annual taxable income: $90,000

- Eligible tax deductions: $5,000

Your taxable income becomes:

$90,000 – $5,000 = $85,000

The ATO then calculates your tax based on the reduced taxable income of $85,000.

The actual tax saving depends on your marginal tax rate, meaning a $1,000 deduction does not result in a $1,000 refund. Instead, the tax benefit is equal to the tax you would have paid on that $1,000.

Common Tax Deductions Australians Can Claim

Depending on your circumstances, common deductions may include:

Work-Related Expenses

Where the ATO rules are satisfied, employees may claim expenses such as:

- Tools and equipment

- Protective clothing

- Uniforms

- Professional memberships

- Union fees

- Self-education expenses directly related to current employment

- Home office running expenses

- Motor vehicle expenses (where eligible)

The expense must:

- Relate directly to earning your income.

- Be paid by you and not reimbursed by your employer.

- Be supported by appropriate records.

Investment Property Expenses

Property investors may be able to claim deductions for expenses including:

- Loan interest

- Property management fees

- Council rates

- Water charges

- Insurance premiums

- Repairs and maintenance (where immediately deductible)

- Depreciation (subject to applicable rules)

Investment Expenses

Investors may also claim certain costs associated with earning assessable income, including:

- Interest on investment loans

- Investment advice fees (where deductible under current law)

- Ongoing portfolio management fees in some circumstances

Charitable Donations

Donations made to organisations endorsed as Deductible Gift Recipients (DGRs) may also be tax deductible.

What Is a Tax Offset?

A tax offset (sometimes called a tax rebate) works differently.

Instead of reducing your taxable income, a tax offset directly reduces the amount of tax you have to pay after your tax liability has been calculated.

This means tax offsets generally provide a dollar-for-dollar reduction in your tax payable, subject to the rules that apply to the specific offset.

For example:

- Tax payable before offset: $4,500

- Eligible tax offset: $500

Final tax payable:

$4,500 – $500 = $4,000

Unlike deductions, the value of a tax offset does not depend on your marginal tax rate.

Common Tax Offsets Available in Australia

Eligibility depends on your personal circumstances and the income year. Some of the more common offsets include:

Private Health Insurance Rebate

Eligible taxpayers with private hospital cover may receive assistance through the Private Health Insurance Rebate, which is income-tested and can be claimed as a reduction in premiums or through the tax system.

Seniors and Pensioners Tax Offset (SAPTO)

Eligible seniors and age pensioners may qualify for the Seniors and Pensioners Tax Offset (SAPTO), which can reduce or eliminate the amount of tax payable if income falls within the applicable thresholds.

Zone and Overseas Forces Tax Offset

Taxpayers living or working in eligible remote areas, or serving in qualifying overseas defence operations, may be entitled to the Zone or Overseas Forces Tax Offset, subject to eligibility requirements.

Superannuation-Related Tax Offsets

Some taxpayers may be entitled to offsets relating to eligible superannuation contributions, including the superannuation tax offset for a low-income spouse where legislative requirements are met.

Tax Deductions vs Tax Offsets: What’s the Difference?

| Feature | Tax Deduction | Tax Offset |

| Reduces taxable income | ✔ Yes | ✘ No |

| Reduces tax payable directly | ✘ No | ✔ Yes |

| Value depends on marginal tax rate | ✔ Yes | ✘ Generally No |

| Claimed in tax return | ✔ Yes | ✔ Yes |

| Subject to eligibility rules | ✔ Yes | ✔ Yes |

Which Saves More Tax?

There is no universal answer. A tax offset often provides a more direct reduction in tax payable because it is generally applied dollar-for-dollar. However, substantial tax deductions can also generate significant tax savings, particularly for taxpayers on higher marginal tax rates.

The overall benefit depends on:

- Your taxable income.

- Your marginal tax rate.

- Your eligibility for particular offsets.

- The amount of deductible expenses you incur.

Both deductions and offsets can play an important role in reducing your overall tax liability.

Common Misunderstandings About Tax Deductions

Many Australians incorrectly believe:

“If I spend $1,000, I’ll get $1,000 back.”

This is incorrect. A deduction reduces taxable income—not your tax bill by the amount spent.

“Everything I buy for work is deductible.”

No. The expense must satisfy the ATO’s deduction rules and have a direct connection with earning your assessable income.

“I don’t need receipts.”

Incorrect. The ATO requires taxpayers to keep appropriate records to support most deductions.

“A tax offset and deduction are the same thing.”

They are different. One reduces taxable income; the other reduces tax payable.

Why Professional Advice Can Make a Difference

Australia’s tax system contains numerous deductions, offsets, concessions and eligibility rules that vary depending on your individual circumstances.

A registered tax agent can help you:

- Identify deductions you’re entitled to claim.

- Determine whether you’re eligible for tax offsets.

- Ensure your return complies with ATO requirements.

- Maintain appropriate records.

- Avoid common errors that may delay processing or result in amendments.

For taxpayers with investment properties, businesses, trusts, capital gains or multiple income sources, professional advice can be particularly valuable.

Conclusion

Although tax deductions and tax offsets both help reduce the amount of tax you pay, they operate in fundamentally different ways.

Tax deductions reduce your taxable income, meaning the value of the deduction depends on your marginal tax rate. Tax offsets, on the other hand, reduce the tax payable after your tax has been calculated and often provide a direct dollar-for-dollar reduction, subject to eligibility criteria.

Understanding this distinction can help you better interpret your tax return, avoid common misconceptions and make informed financial decisions throughout the year. If you’re unsure which deductions or offsets apply to your circumstances, consulting a registered tax professional or referring to the ATO’s official guidance can help ensure you receive every tax benefit you’re legally entitled to while remaining fully compliant with Australian tax law.

Frequently Asked Questions

What’s the main difference between a tax deduction and a tax offset?

A tax deduction reduces your taxable income before tax is calculated, while a tax offset reduces the amount of tax payable after your tax liability has been worked out.

Does a tax deduction give me a dollar-for-dollar refund?

No. The value of a deduction depends on your marginal tax rate. A $1,000 deduction reduces your taxable income by $1,000, not your tax bill by $1,000.

Are tax offsets better than deductions?

Not necessarily. Tax offsets generally reduce tax payable directly, but deductions can also provide substantial tax savings depending on your income and marginal tax rate.

Can I claim both deductions and tax offsets?

Yes. Many taxpayers are eligible to claim deductions as well as tax offsets, provided they meet the relevant eligibility requirements.

Do I need receipts for tax deductions?

Generally, yes. The ATO requires taxpayers to keep records such as receipts, invoices, bank statements or other evidence to support deductible expenses.

Are all tax offsets refundable?

No. Some tax offsets are non-refundable, meaning they can reduce your tax payable to zero but generally cannot create a refund beyond the tax you’ve paid. The rules differ depending on the specific offset.

Should I use a registered tax agent?

If your tax affairs are complex or you’re unsure about your eligibility for deductions or offsets, a registered tax agent can help ensure your return is accurate and compliant while identifying legitimate tax-saving opportunities.

Sources

- Australian Taxation Office (ATO)

- CPA Australia

- Chartered Accountants Australia and New Zealand (CA ANZ)

How can we help?

If you have any questions or would like further information, please feel free to give our office on 08 9221 5522 or via email – info@camdenprofessionals.com.au or arrange a time for a meeting so we can discuss your requirements in more detail.

General Advice Warning

The material on this page and on this website has been prepared for general information purposes only and not as specific advice to any particular person. Any advice contained on this page and on this website is General Advice and does not take into account any person’s particular investment objectives, financial situation and particular needs.

Before making an investment decision based on this advice you should consider, with or without the assistance of a securities adviser, whether it is appropriate to your particular investment needs, objectives and financial circumstances. In addition, the examples provided on this page and on this website are for illustrative purposes only.

Although every effort has been made to verify the accuracy of the information contained on this page and on this website, Camden Professionals, its officers, representatives, employees, and agents disclaim all liability [except for any liability which by law cannot be excluded), for any error, inaccuracy in, or omission from the information contained in this website or any loss or damage suffered by any person directly or indirectly through relying on this information.

Recent Comments